25 August 2020

Vietnam has retained exceptional growth despite being affected by various economic crises over the last 25 years. Besides being considered the sector of choice for investors in Vietnam, property remains the safest and most effective investment channel.

Even though COVID-19 might last into early 2021, Savills anticipates a strong recovery from 2021 to 2022 and beyond. Moreover, effective and timely government support, as shown through its effective pandemic response and recent stimulus policies, will provide further powerful leverage for real estate businesses and the national economy.

Since the mid-90s, the domestic property market has had a pattern of impressive growth, brief downturn, and recovery. However, the COVID-19 pandemic in the first half of 2020 negatively affected the market in an unprecedented manner.

1995 to 1998: Stabilising relations with the United States and officially joining ASEAN in 1995 marked successful milestones.

The transition from a centrally planned to a market-driven economy was establishing a robust platform for lasting change and growth.

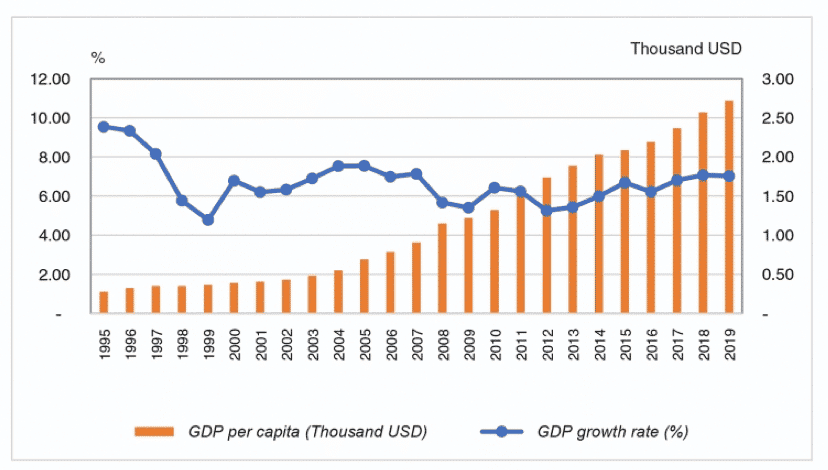

The General Statistics Office (GSO) shows growth in 1995 was 9.54 percent and 9.34 percent in 1996, correlating with per capita GDP increasing from $277 in 1995 to $324 in 1996.

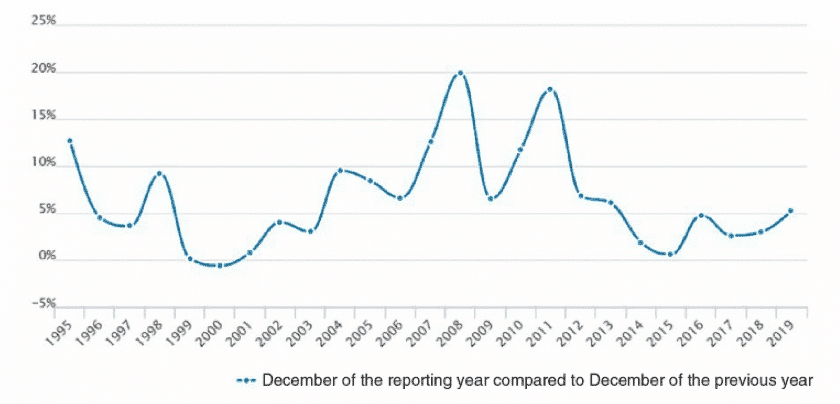

Inflation was reined in from 12.7 percent in 1995 to 4.5 percent in 1996 and 3.6 percent in 1997.

At the same time, GDP growth and increased consumer confidence resulted in rising land prices as the property market started to show signs of promise.

The domestic market then entered a prolonged slowdown with the onset of the Asian Financial Crisis in 1998 impacting the nascent market economy.

GSO data shows 5.76 percent economic growth in 1998, while inflation reached 9.2 percent. However, the limited market opening resulted in a proactive government response, which helped successfully manage the crisis and enable a strong foundation for future growth.

1998–2008: The early years of the 21st century were characterised by further economic integration.

In 2001, the Vietnam-US Bilateral Trade Agreement (BTA) was ratified, followed by Vietnam becoming a member of the World Trade Organisation (WTO) in 2006.

Back in 2000, Vietnam was considered the next “Asian Tiger” economy, with per capita GDP growing to $396, compared to $328 in Laos and $283 in Cambodia. New national economic and macroeconomic policies saw 6.79 percent GDP growth in 2000, up to 6.89 percent in 2001, followed by robust GDP growth averaging 8.23 percent per year from 2004 to 2007.

Property market fluctuations inevitably followed. National economic indicators reflected a strong global economy, increased confidence in local economic recovery, and steady increases in foreign direct investment (FDI).

Furthermore, effective government policies contributing to market performance saw land prices ramp up.

Significant price growth driven by increasing transactions led to the property market becoming everyone’s favourite investment channel.

However, land prices increasing significantly over the two most frantic periods of 2001–2003 and 2007–2008 started to exclude lower-income investor participation from Ho Chi Minh City and Hanoi.

Per capita GDP and GDP growth, 1995–2019

Per capita GDP and GDP growth, 1995-2019 (Source: General Statistics Office)

Property inventory in 2012 was over VND100 trillion ($4.35 billion), while property enterprises under bad debt increased. Rapidly rising inflation forced the State Bank to tighten monetary policies.2008–2018: Growth punctuated by a slowdown continued. In mid-2008, effects from the Global Financial Crisis led to a downward cycle in the domestic property market, and land prices dropped by up to 40 percent.

The government, by revising policies and releasing economic stimulus packages to attract investment, helped successfully navigate the crisis.

Social-housing-focused companies helped responsibly modify social housing policies and pricing. Together with government-supported VND30 trillion ($1.3 billion) credit packages, a real estate recovery started, but inventory remained high. The market started to demonstrate sustained growth. Property segments bursting into life, such as hotels and second homes, ushered in new economic potential for provinces gifted with favourable geography and natural appeals, such as Ba Ria-Vung Tau, Phu Quoc Island, Nha Trang, Halong, and in particular Danang.

Vietnam CPI, 1995–2019 (Source: The General Statistics Office)

2018 to 2020: The latest World Bank report finds Vietnamese economic growth over the last two years has been mainly driven by high consumer demand and manufacturing-based export growth.

Economic data indicating 7 percent real GDP growth in 2019 reflected one of the fastest-growing economies in the region.

While globalisation has positively affected Vietnam, the COVID-19 pandemic has caused extensive damage to global and local economies.

Fortunately, early and decisive measures from the government meant Vietnam was far less affected than other countries in the region. While fiscal policies were stable, with GDP growth reaching 3.8 percent in the first quarter of 2020, the pandemic, as it expanded, became more unpredictable.

The Asian Development Bank (ADB) estimates that Vietnam’s GDP growth will reach 4.1 percent in 2020. Although this is 0.7 percent lower than their forecast in April, it remains the highest forecast growth in Southeast Asia. The World Bank anticipates 3 percent GDP growth in 2020, and its 6.8 percent growth forecast for 2021 shows confidence remains high in the local economy.

The Vietnamese economy is primed for recovery, and the real estate sector is set to be one of the key beneficiaries in 2021 and beyond. – Savills Vietnam